You notice it when a stone chips your windshield, or a mirror clips a tight garage post. Repairs cost more now, and even a small claim can raise questions later. For truck and SUV owners, the bills can climb fast.

If you are sorting options, it helps to work with an agency that deals with common cases daily. Many California drivers start with IIS Insurance because it handles auto needs like SR 22 filings and multi vehicle coverage. That kind of experience matters when details decide how a claim pays out.

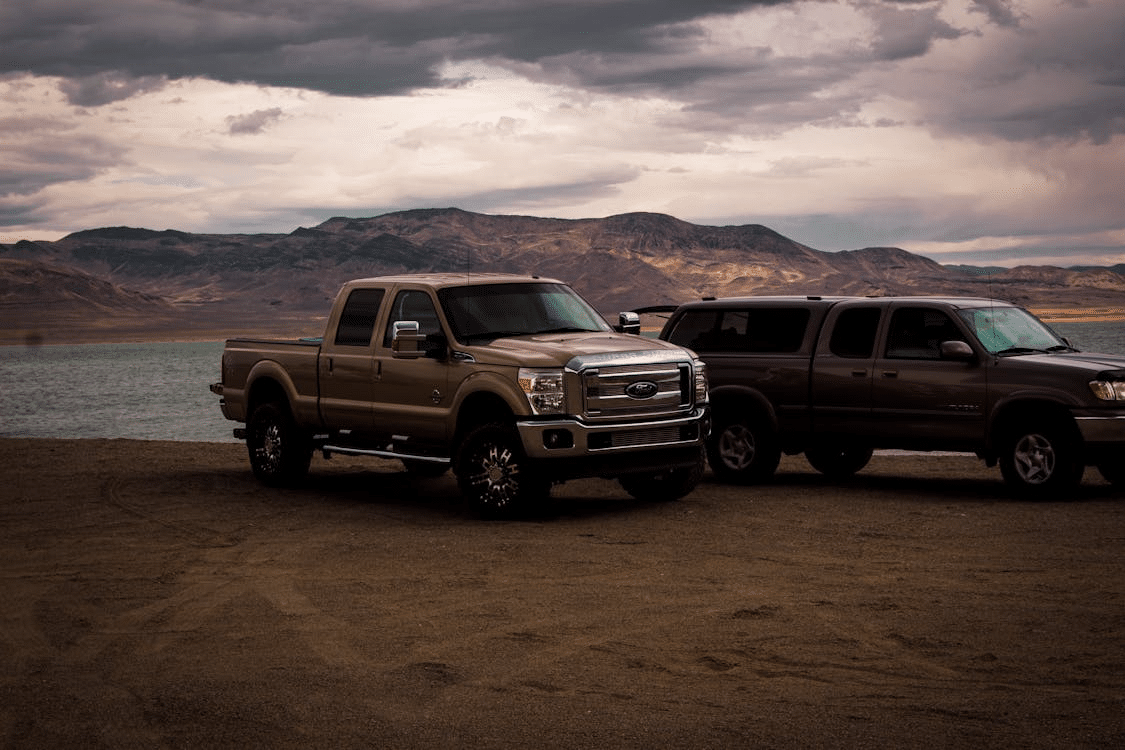

Match Coverage To How You Use The Vehicle

A commuter SUV and a work truck face different risks on the same road. Towing, hauling, and jobsite parking raise the odds of damage and theft. Those uses can also change how insurers rate the vehicle.

Start by listing what the vehicle does in a normal week, not a perfect week. Include towing frequency, average miles, and where it sleeps at night. Add any rideshare, delivery, or business use if it happens even part time.

If your setup is not stock, write down the changes and their rough value. Lift kits, wheels, bed covers, toolboxes, and winches can change repair costs. If they are not listed, you may get paid like they never existed.

Useful details to gather before quotes:

- Current mileage and typical weekly miles

- Towing weight range and trailer type

- Garage, driveway, or street parking address

- Aftermarket parts list with photos and receipts

Compare Protection Pieces, Not Just The Monthly Price

Liability pays for harm you cause others, and it is not optional in most states. Collision and comprehensive protect your own vehicle from crashes, theft, weather, and vandalism. Uninsured and underinsured coverage matters when the other driver cannot pay.

Many drivers pick a low premium and miss the parts that matter in a real claim. A higher deductible can lower cost, but it also raises your cash burden after a loss. Think about what you could pay within a week, without adding debt.

You also want to know how your state rules shape the quote. In California, rules and required disclosures can affect how insurers set rates and present coverage. The California Department of Insurance has a plain guide that helps you compare common parts side by side.

When comparing quotes, focus on the numbers that move real payouts:

- Liability limits that match your assets and income risk

- Deductibles you could cover without missing rent or payroll

- Rental and roadside options that fit your daily driving needs

Ask How Claims Work For Repairs, Parts, And Shops

Two policies can look similar until you hit a claim and need a shop slot fast. Ask whether the policy uses original parts, aftermarket parts, or a mix, because it can affect fit. That matters for modern bumpers, sensors, and camera systems.

Also ask how the insurer handles labor rates in your area. If the policy assumes lower rates than local shops charge, you may see delays and extra calls. Clear answers here can save days of back and forth later.

If you use your truck for work, downtime can cost more than the damage. Ask about rental limits, daily caps, and how long coverage lasts. If you tow, ask if a rental truck is covered, or only a small car.

Questions worth asking before you buy:

- Do you cover ADAS sensor calibration after a bumper or windshield replacement?

- Is glass covered with a separate deductible, or the full comprehensive deductible?

- Can I use my own shop, and how do you handle supplement approvals?

Know When You Need SR 22, And Avoid Coverage Gaps

An SR 22 is not insurance, it is a state filing that proves you carry required coverage. Drivers may need it after certain violations, license issues, or lapses. The filing is time sensitive, and a missed payment can create a new problem.

If you think an SR 22 might apply, ask early and get the timing right. You want the policy start date and filing date to match what the DMV expects. You also want to know how long the filing must stay active.

Coverage gaps also matter even without an SR 22. A lapse can raise rates, reduce options, or trigger fees when you restart. If you are switching carriers, overlap start and end dates so there is no dead space.

Common gap risks to watch for:

- Canceling early because a new card arrived, before the new policy is active

- Letting auto pay fail after a card change or bank hold

- Removing a vehicle during repairs, then forgetting to reinstate full coverage

Recheck The Policy After Big Changes And Each Renewal

Insurance is not a one time choice, because your risk picture changes. A new commute, a teen driver, or a new address can change pricing and coverage needs. Even a single speeding ticket can shift renewal terms.

If you add a trailer, camper, or accessories, confirm they are covered the way you think. Ask whether your policy covers the trailer itself, its contents, and liability while towing. If you bought a used SUV, check whether its safety tech affects pricing.

It also helps to keep an eye on recalls and safety fixes. Some repairs are free, and they can prevent the kind of crash that starts a claim. The NHTSA recall lookup lets you check open recalls by VIN in minutes.

A simple renewal routine keeps you from paying for the wrong setup:

- Review drivers, miles, and use, then update the policy details

- Confirm deductibles and limits still match your budget and risk

- Save photos and receipts for added equipment and recent upgrades

A Policy Check That Pays Off

The strongest policy is the one that still makes sense on a rough day, after a claim, and not just on a calm billing cycle. Start with how you really drive, where you park, what you tow, and what you have added to the truck or SUV. Then line up limits and deductibles with what you could cover quickly, and make sure the claim process matches how you would repair the vehicle in your area.

After that, treat renewals like a quick equipment check, not a chore you rush through. Revisit the details after a move, a new commute, a new driver, or a bigger trailer, and keep photos and receipts for any upgrades. If you do that, you spend less time arguing over fine print later, and more time driving with a plan you can count on.

{kind=link}

{kind=link}

{kind=link}