Pickup trucks are built to do more: tow trailers, haul tools, handle rough terrain, and often double as work vehicles. That versatility is exactly why insurance claims involving trucks can become more complicated than many drivers expect.

Many truck owners assume their policy automatically covers everything attached to the vehicle or everything they use it for. In reality, insurance coverage can depend on how the truck is used, what equipment has been added, and even what’s being transported in the bed.

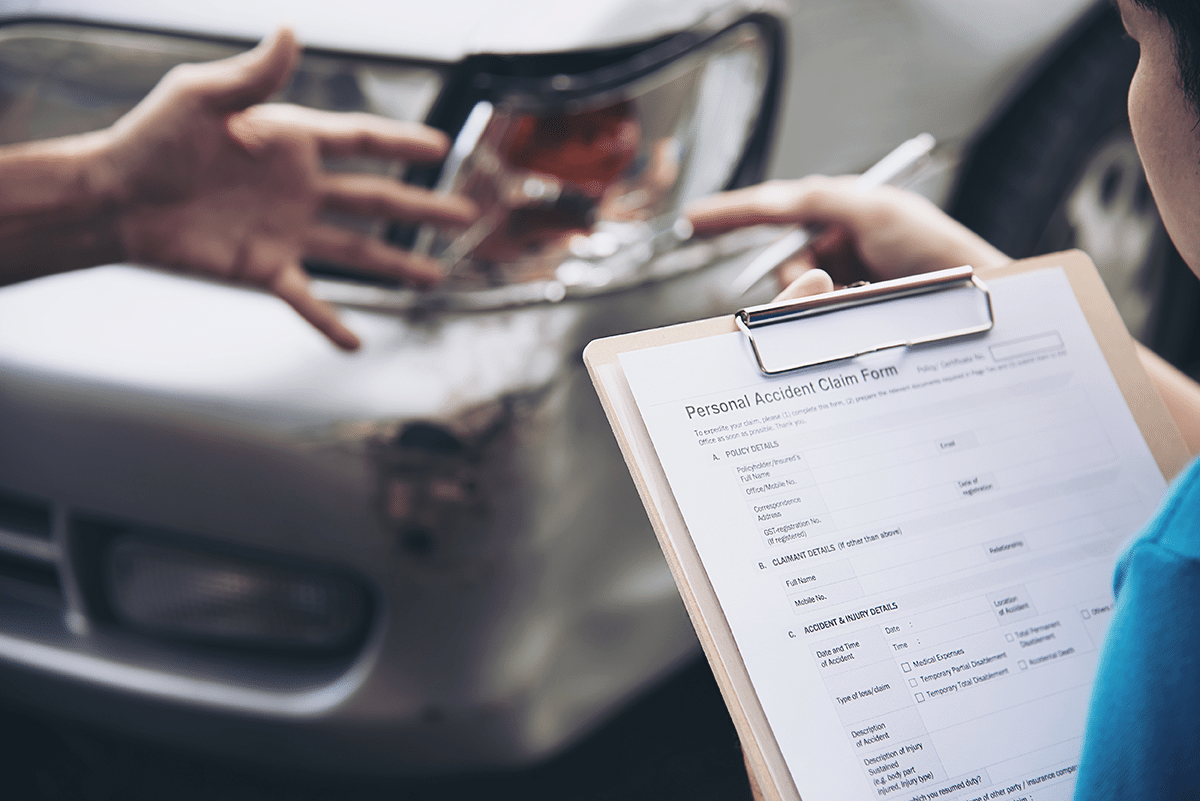

Over the years, we’ve seen situations where drivers believed they were fully covered—only to discover after an incident that their policy had limitations they didn’t know about.

Before getting into specific coverage gaps, it helps to understand one important factor.

Why Truck Insurance Claims Are Often More Expensive

Pickup trucks are generally larger and heavier than passenger cars, and that alone can influence insurance costs. But the bigger reason many claims become expensive is how trucks are used.

According to the Insurance Institute for Highway Safety (IIHS), pickups are among the most common vehicles used for towing and work-related transportation in the U.S. That means claims often involve trailers, cargo, or additional equipment, which increases both complexity and potential damage costs.

Repair costs for trucks have also risen significantly in recent years. Modern pickups often include:

- aluminum body panels

- integrated sensors and cameras

- advanced driver-assistance systems

- electronic tailgates and safety technology

Even minor damage can require recalibration of safety systems or replacement of expensive parts.

Data from the National Highway Traffic Safety Administration (NHTSA) also shows that pickup trucks and other light trucks play a significant role in towing activity and trailer-related crashes in the United States, based on analyses from the agency’s Fatality Analysis Reporting System (FARS) and Crash Report Sampling System (CRSS).

Because of these factors, insurers tend to review truck-related claims more closely, especially when modifications, towing, or cargo are involved. That’s often when drivers start discovering the fine print in their policies.

Aftermarket Mods May Not Be Fully Covered

Pickup trucks are one of the most frequently modified vehicle types in the country. Common upgrades include:

- lift kits

- oversized tires

- upgraded suspension

- aftermarket bumpers and lighting

- custom wheels

- performance upgrades

However, many insurance policies only cover a vehicle in its original factory configuration. If a truck with thousands of dollars in upgrades gets damaged, the insurance company may reimburse only the value of the original parts unless those modifications were specifically listed in the policy.

For example, a truck with a lift kit, upgraded suspension, and larger tires could have $8,000–$15,000 in modifications. If the vehicle is involved in a claim and those upgrades weren’t disclosed to the insurer, coverage for those components may be limited.

For truck owners who invest in modifications, it’s often worth discussing those upgrades with an insurance provider so they can be properly documented.

Towing Can Create Coverage Gaps

Many pickup owners regularly tow:

- campers

- boats

- utility trailers

- construction equipment

Towing is one of the reasons many drivers choose a pickup truck. According to transportation data from the U.S. Department of Transportation, more than 30 million Americans tow trailers each year, with pickup trucks accounting for a large share of those vehicles.

At the same time, surveys suggest that many truck owners don’t tow as often as people might assume. A 2019 Strategic Vision study found that about 75% of pickup owners tow once a year or less, and roughly one-third report never using the truck bed for hauling at all.

That mix of occasional towing and everyday driving means many owners don’t think much about how their insurance handles trailers until a situation arises where coverage questions come up.

That assumption isn’t always accurate.

Some auto policies may cover liability while towing but not damage to the trailer itself. In other cases, the trailer might be covered only if it is specifically listed in the policy.

Coverage may also depend on factors such as:

- trailer weight

- whether the trailer is owned or rented

- whether the truck is used for personal or business purposes

Cargo inside the trailer is often treated separately as well. For truck owners who frequently tow boats, campers, or work trailers, reviewing how a policy treats trailers can help avoid surprises.

Using Your Truck for Work Can Affect Coverage

Pickup trucks are commonly used for side jobs and small businesses.

Examples include landscaping, construction work, equipment transport, mobile repair services, and deliveries. The U.S. Small Business Administration notes that millions of small businesses rely on light-duty trucks for daily operations.

However, many standard auto insurance policies are designed primarily for personal vehicle use.

If a truck insured under a personal policy is involved in a situation while being used for commercial activity, the insurance company may review whether the policy applies to that use. This doesn’t automatically mean coverage will be denied, but it can complicate the claim process.

Truck owners who regularly use their vehicle for work may benefit from reviewing whether their policy adequately reflects how the truck is actually being used.

Cargo in the Truck Bed Isn’t Always Covered

Pickup trucks often carry valuable items in the bed, including power tools, generators, building materials, camping or outdoor equipment.

In many cases, auto insurance covers the vehicle itself, but not necessarily the items being transported.

Coverage for cargo can depend on several factors, including whether the items are considered personal property or work equipment.

For example:

- personal items may fall under homeowners’ or renters’ insurance

- work tools may require commercial coverage or equipment insurance

Understanding the difference between vehicle coverage and property coverage can help prevent confusion if something is damaged or stolen.

What Happens If an Insurance Claim Is Disputed?

When trailers are involved, determining responsibility can become more complicated, especially if multiple vehicles or pieces of equipment are part of the situation. In more serious cases, drivers may need legal guidance to sort through insurance coverage, liability questions, and negotiations with insurers.

You can consult a lawyer to look together at what really happened, review the insurance policies involved, and figure out who may actually be responsible. If you’re wondering how that process works, understanding what a truck accident lawyer does can give drivers a clearer picture of how these claims are handled, and what you can do if an insurance company starts pushing back or trying to pay out less than the claim may be worth.

Final Thoughts

Pickup trucks are incredibly versatile vehicles. They’re built for work, recreation, and everything in between.

That flexibility is part of their appeal, but it can also make insurance coverage more complex than many drivers expect.

Taking a few minutes to review your policy, especially if you tow regularly or modify your truck, can go a long way toward preventing unpleasant surprises later.

And if a claim ever becomes complicated, understanding your coverage and options can make the process far less stressful.

{kind=link}

{kind=link}

{kind=link}